%20(3).png)

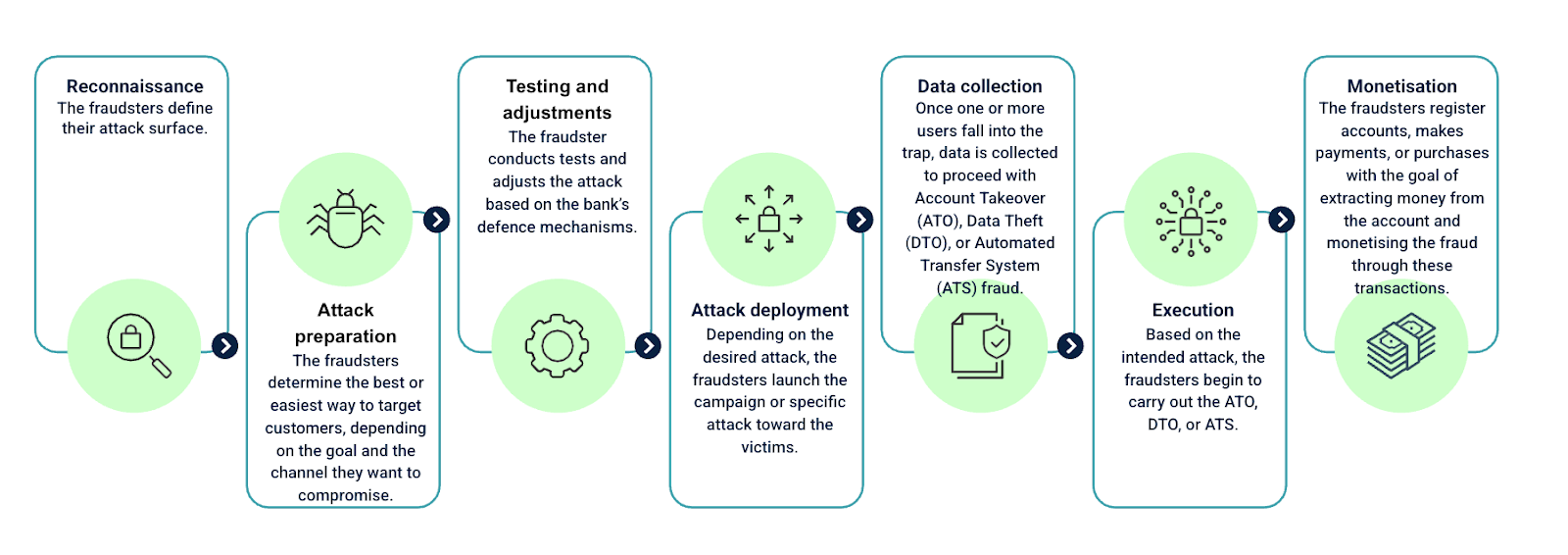

Digital fraud has changed. Attacks are no longer single events. They unfold across sessions, channels, devices, and time. Yet most fraud tools still treat each activity as if it exists in isolation. That gap is where modern fraud succeeds.

Attack Pattern Recognition (APR) was created to close that gap.

APR allows banks to see how an attack actually works, not just the moment it surfaces. Instead of scoring a transaction and moving on, APR rebuilds the whole digital journey and reveals the tactics that made the fraud possible.

This article explains what APR is, how it works, and why it matters for banks that want to prevent fraud earlier in the chain.

What APR means in practice

At its simplest, APR is a method for reconstructing the whole attack sequence. It correlates signals from devices, networks, applications, user behaviour, and session telemetry in real-time, then identifies how the activities link together.

The outcome is not a score. It is a factual narrative of what happened. That narrative contains deterministic signals, such as:

- Malware present

- Remote access active

- Session integrity broken

- Parallel session detected

- Suspicious manipulation during login or transfer

These are not statistical guesses. They are observable events that can be verified, explained, and acted on.

APR turns fraud detection into event reconstruction.

Why this matters more than ever

Modern fraud is designed to exploit the blind spots between tools. A session that looks benign to the transaction monitoring system might already be compromised. A device that appears trusted may be running remote access tools. Behaviour that seems normal can be scripted or assisted by malware.

When each layer operates alone, these signals remain disconnected. APR turns them into a single story.

That shift delivers three practical benefits:

- Earlier detection, before money moves

- Stronger evidence for operations, audit, and regulatory review

- Less manual investigation effort, because the system pre-correlates the facts

Banks no longer have to guess. They can see what happened.

.png)

How APR supports safer automation and responsible AI

APR does not replace analysts. It makes them scalable.

Because every decision is built on deterministic signals, automated actions become safer. Approvals can be tied to evidence rather than confidence scores, and AI models can summarise and reason over events without turning the system into a black box.

If a payment is held or a session is blocked, the system can show exactly which events triggered the action. That makes automation explainable, auditable and aligned with current supervisory expectations in the UK and Europe.

APR is the data foundation that allows AI to be useful without becoming opaque.

Where APR fits in the wider fraud strategy

APR sits beneath the entire fraud stack, not on top of it. It enriches every stage of the digital journey, from login to logout, and connects risk signals that would otherwise remain isolated. It bridges cyber and fraud functions, providing both teams with the shared context they have been missing.

It is not a new typology. It is a new way of understanding how attacks work, regardless of the label attached later.

Banks use APR to:

- Investigate faster, because the evidence is already organised

- Reduce false positives, because signals reinforce each other

- Improve customer experience, because interventions are based on certainty, not suspicion

- Strengthen compliance and model governance

- Prevent incidents that would have looked normal in a transaction-only model

The forward view

The industry has spent a decade increasing scale, speed, and model complexity. That has delivered better scoring, but not better understanding. Prevention now depends less on data volume and more on the ability to interpret it in context.

Attack Pattern Recognition is the step that turns data into knowledge. It reveals what the attacker did, how they did it, and where the next opportunity will appear. That is the difference between reacting to fraud and getting ahead of it.

APR is not another layer. It is the connective fabric that makes fragmented systems coherent and fraud defence predictable.

That is why it sits at the centre of Cleafy’s approach.

.png)

%20(1)%20copia%203.png)

%20(2).png)