%20copia%207.png)

A convincing voice. A sense of urgency. And moments later, the money’s gone.

This is not just a nightmare scenario — it’s the reality of Authorised Push Payment (APP) fraud. With the rise of real-time digital payments, these scams are increasing rapidly. According to TechTarget, they're expected to surge even more by 2026. To fight back, banks are deploying tougher anti-fraud controls. But too often, these solutions disrupt genuine customer actions, creating tension between safety and usability.

So, how can banks keep fraud at bay while preserving a smooth digital experience?

In this article, we explore the anatomy of APP fraud, how scammers exploit trust, and how banks can strike the perfect balance between protection and convenience.

What is APP fraud?

APP fraud happens when someone is tricked into sending money to a fraudster’s account. Unlike unauthorised access attacks, victims of APP fraud willingly initiate the transaction — convinced they are paying a legitimate party. That’s what makes it so dangerous. Once the money is gone, it's often unrecoverable.

Unlike traditional fraud, these scams don’t rely on stolen passwords or hacked devices — they rely on stories. And increasingly, they’re supported by technology designed to make those stories stick.

Common types of APP scams

APP scams take many forms, they’re carefully planned and supported by infrastructure:

- A ‘seller’ offers a deal too good to be true — a gadget, a car, even a holiday — and vanishes after payment.

- Someone claiming to be a financial adviser pitches a high-return investment that doesn’t exist.

- An online love interest builds trust over weeks or months, then fakes an emergency needing urgent funds.

- A business receives an invoice that looks exactly like one from a regular supplier — but the bank details have been swapped.

- A person receives a convincing call from their ‘bank’ urging them to move their funds to a ‘secure account.’

What connects these? Human persuasion, social engineering reinforced by technical tools like spoofed numbers, fake domains, and remote access malware. And it works.

How APP scams work: A coordinated setup

The mechanism of APP fraud

APP scams rely on more than impersonation — they use calculated psychological pressure. Scammers leverage urgency (“Act now or lose your money”), fear (“Your account’s been compromised”), and even authority (“This is the police”) to override a person’s natural scepticism.

They dig through hacked emails, mine social media, and gather enough context to sound completely convincing. And with AI-driven voice cloning and deepfake tools on the rise, that illusion is only getting stronger.

Real-world examples of APP fraud

Consider the retiree who got a call from someone claiming to be their bank, reporting a fraud attempt. Urged to move their funds quickly, they did — straight into the fraudster’s account.

Or the student in a long-distance online relationship who, after months of chatting, sent thousands to help with a ‘medical emergency’ — only to discover the entire romance was a ploy.

Even experienced professionals have been duped. One executive received what looked like a routine email from their CEO requesting a wire transfer. The message was perfect — except it was fake. By the time they realised, the funds were long gone.

The impact of APP fraud on victims and online banks

Financial and emotional consequences for victims

For the victims, the damage goes beyond financial. Not only is it difficult — often impossible — to get their money back, but the emotional fallout can be severe. Shame, embarrassment, and anxiety are common. Many victims lose trust not just in their bank but in themselves.

Repercussions for financial institutions

Banks are feeling the pressure, too. Regulations are tightening, and expectations around customer protection are rising. The cost of reimbursements, combined with increased demand for support and investigation, strains resources and reputations.

A single high-profile fraud case can undermine years of brand trust. Customers don’t want apologies — they want security.

Why traditional fraud tools fall short

Most fraud detection systems focus on what's happening at the transaction. But APP scams start long before that. By the time a flagged payment is reviewed, the manipulation has already worked.

These scams don’t stand out by device or location alone. It’s the combination of behaviours - and their timing - that signal something’s off.

That’s where banks need new visibility: earlier, broader, and based on the full digital interaction.

How to prevent and fight APP fraud

Preventative measures for consumers

The first line of defence is awareness. Before acting on any request, users should pause and verify. A quick phone call — using contact details from the official website, not the message — can make all the difference.

People should stay alert to red flags: pressure to act fast, requests to keep the transaction secret, or payment instructions that differ from usual practices. Banks offer security features like transaction alerts and biometric logins — but they only work if customers use them.

How can online banks protect themselves with technological solutions

Banks are now moving beyond basic fraud detection toward smarter, more adaptive systems. AI and machine learning can monitor behaviour patterns in real-time, flagging anomalies such as unusual payment amounts or activity at odd hours. But detecting fraud is only half the battle.

What’s often missing is context. Fraud doesn’t always look suspicious in a vacuum. But what if you could link subtle hints across sessions, users, and time?

How Cleafy protects your customers from APP fraud while minimising the impact on their online experience

Traditional fraud detection is fragmented, like piecing together a book from scattered words. It focuses on isolated events, missing the broader context of an attack. Financial institutions require a holistic approach that:

- Analyses all digital interactions in real-time.

- Constructs a complete fraud narrative to identify attack patterns.

- Proactively identifies threats to prevent fraud before transactions occur.

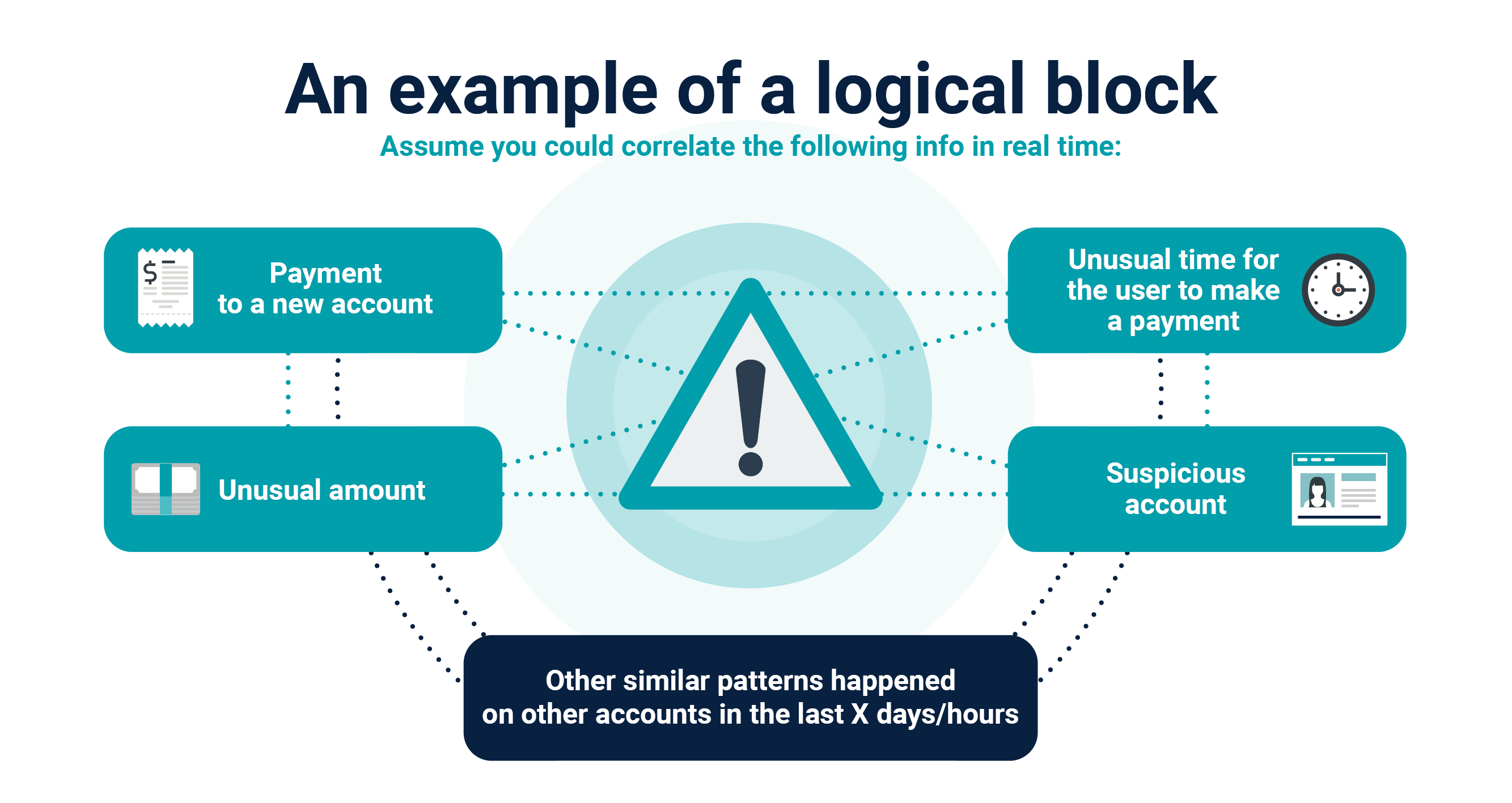

Cleafy goes beyond isolated threat alerts by reconstructing the entire attack narrative in real-time, giving banks and FIs complete situational awareness connecting different behaviours such as:

A new payee. An unusual time. A larger-than-normal amount. Other similar patterns occur across different users.

Alone, none of these may signal danger. Together, they paint a different story.

When a high-risk scenario is detected, Cleafy doesn’t necessarily block the transaction outright. Instead, it prompts the user: “Are you sure you know this person? We’ve seen similar fraud attempts recently.”

This simple intervention keeps the user in control — but gives them pause to reflect. It’s often enough to stop a scam in its tracks.

Cleafy allows teams to make smarter decisions earlier, based on a broader context resulting inewer blocked transactions for legitimate users, less strain on fraud analysts, and a significantly stronger barrier against scams.

It’s fraud prevention that fits the modern digital experience.

.png)

.png)

%20(2).png)

%20copia%205.png)